WASHINGTON, D.C. — Today the Consumer Financial Protection Bureau (CFPB) unveiled the student loan Payback Playbook, a set of prototype disclosures that outline a path to affordable payments for borrowers trying to avoid student debt distress. The Payback Playbook provides borrowers with personalized information about their repayment options from loan servicers so they can secure a monthly payment they can afford. The Payback Playbook would be available to borrowers on their monthly bills, in regular email communications from their student loan servicers, or when they log into their student loan accounts.

“Millions of consumers needlessly fall behind on their student loan debt, despite their right under federal law to a payment they can afford,” said CFPB Director Richard Cordray. “The Payback Playbook, which has grown out of our joint work with Illinois Attorney General Lisa Madigan and her colleagues, is designed to help ensure student loan servicers provide personalized information, tailored to the borrower’s individual situation. This will help these borrowers take action, stay on track, and steer clear of financial distress.“

View the Payback Playbook prototypes at: https://files.consumerfinance.gov/f/documents/201604_cfpb_student-loan-playbooks-website.pdf

About 43 million Americans owe student loan debt, with outstanding debt estimated at $1.3 trillion. The Department of Education offers numerous plans to borrowers with federal student loans that help make payments more affordable. These include options that let borrowers set their monthly payment based on their income. Repayment plan options for federal loans have expanded in recent years, but record numbers of student borrowers continue to struggle with debt. One out of four student loan borrowers are currently in default or scrambling to stay current on their loans, despite the availability of income-driven repayment options for the vast majority of borrowers.

According to a government audit , 70 percent of federal Direct Loan borrowers in default earned incomes low enough to qualify for reduced monthly payment under an income-driven repayment plan. These findings and the continued problems reported by student loan borrowers raise serious concerns that millions of consumers may not be receiving important information about repayment options or may encounter breakdowns when attempting to enroll.

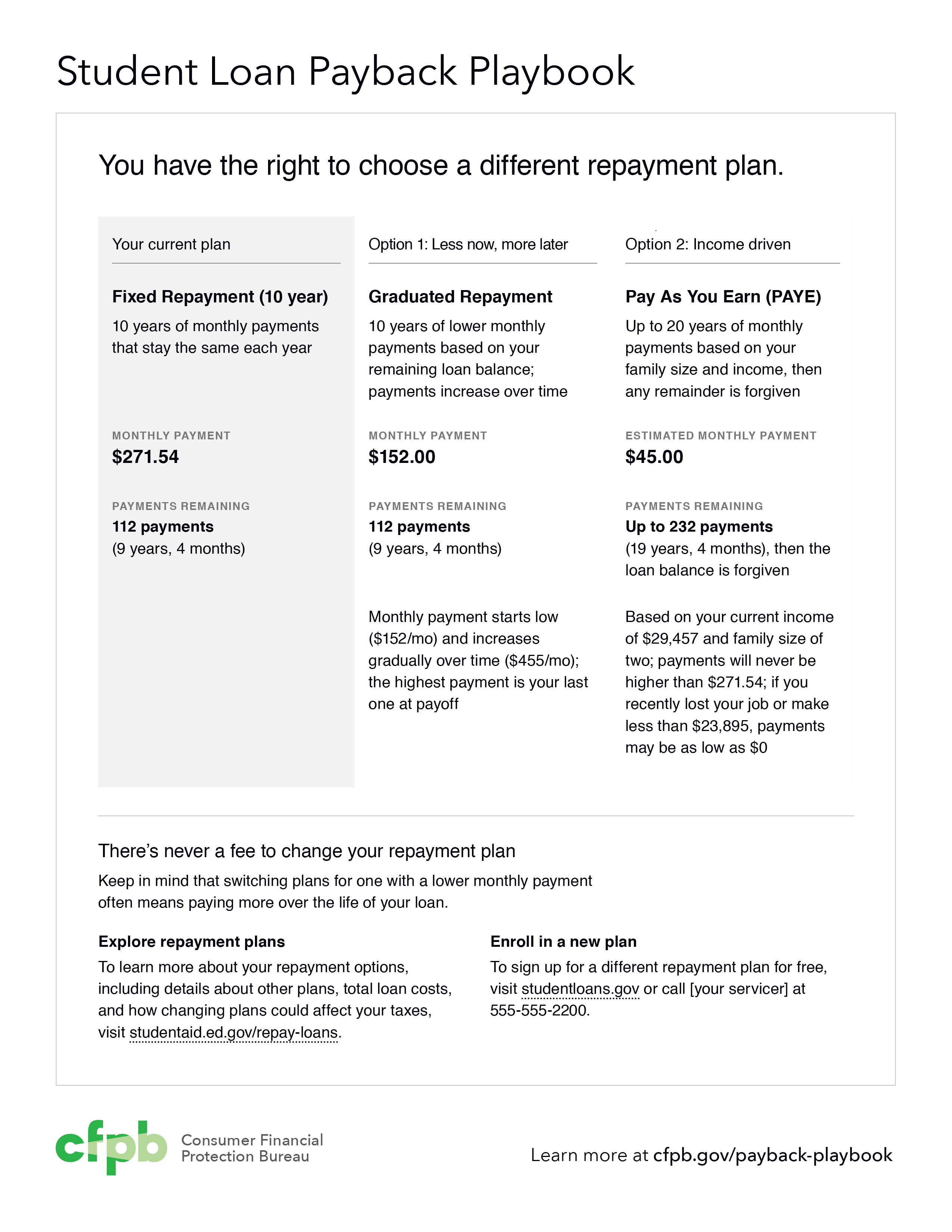

Prototype Student Loan Payback Playbook

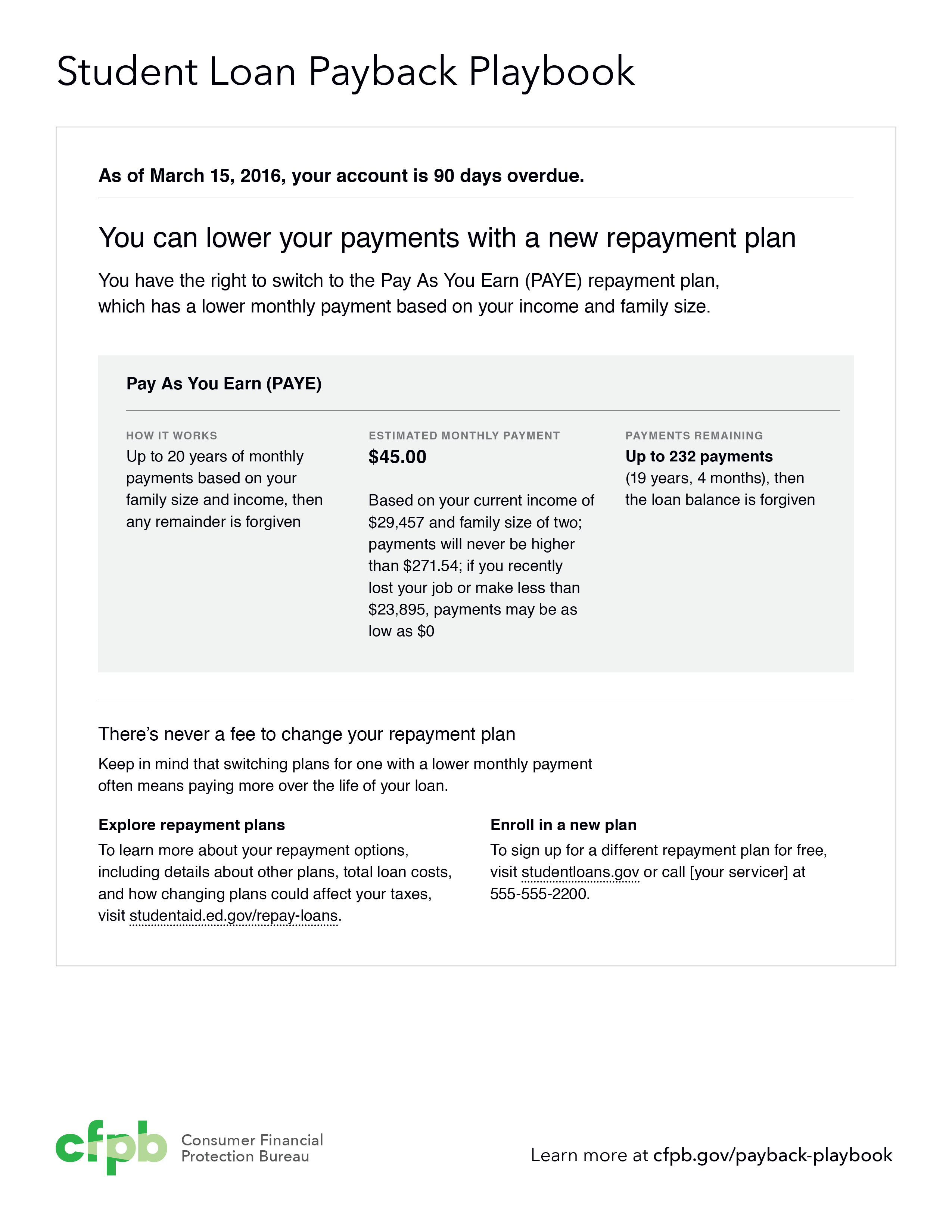

The first-of-its-kind prototype student loan Payback Playbook outlines repayment options for consumers who may be struggling to keep up with their monthly payment or trying to choose among dozens of plans. The Payback Playbook that most borrowers receive from their servicer will help cut through the clutter by clearly presenting three personalized repayment options. Struggling borrowers who have missed a payment or are at risk of default will receive a Payback Playbook that provides a single option with personalized instructions written in plain language describing how to lower their monthly payment. The proposed Payback Playbook features will include:

{kind=link}

{kind=link}

- Personalized payment options: The Payback Playbook would require servicers to provide personalized information tailored to borrowers’ specific circumstances that show what their payments will be under different repayment plans. This information would include the number of payments over the life of the loan, monthly payment amounts, and whether payments will change over time.

- No fine print: The Payback Playbook describes each option using clear, straightforward language that makes it easier for borrowers to understand the different plans, pick one that fits their financial situation, and stay on track.

- Real-time, up-to-date information: The Payback Playbook provides borrowers with updated information when their plans or circumstances change so they can keep on top of their payments. This includes how much longer they need to make payments until their loan is paid off or forgiven.

The Payback Playbook is available online and the public can provide feedback on these prototype disclosures through June 12, 2016. In the coming months, the Department of Education plans to finalize these disclosures, informed by the public feedback shared with the Bureau, to ensure that student loan servicers provide the information borrowers need to obtain monthly payments they can afford. The Department of Education, working with the CFPB, plans to finalize and implement these disclosures as part of the new vision for serving student loan borrowers announced earlier this month.

The public can weigh in starting April 28, 2016 on the Payback Playbook prototypes at: www.consumerfinance.gov/payback-playbook

A copy of the CFPB public request for information is available at: https://files.consumerfinance.gov/f/documents/201604_cfpb_rfi-regarding-student-loan-borrower-communications.pdf

In a related action, the Bureau today also released a new action guide to help military borrowers navigate their student loan repayment options and take advantage of special consumer protections designed to help men and women in uniform manage their debt while serving our country.

Reforming Student Loan Servicing

The CFPB’s development of the prototype Payback Playbook was informed by the ongoing work of state law enforcement agencies and a public inquiry last year. The inquiry identified widespread concerns about student loan servicing practices. Servicers are a crucial link between borrowers and lenders. They manage borrowers’ accounts, process monthly payments, and communicate directly with borrowers. When facing unemployment or other financial hardship, borrowers may contact student loan servicers to enroll in alternative repayment plans, obtain deferments or forbearances, or request a modification of loan terms.

The CFPB’s inquiry into the practices of student loan servicers received more than 30,000 comments from student loan borrowers, servicers, policy experts, and consumer advocates, describing widespread servicing failures that can drive student loan borrowers into default. Consumers reported miscommunication from servicers that caused distress, increased costs, and prevented borrowers from obtaining affordable payments. Also, some borrowers trying to avoid default reported falling prey to debt relief scammers that charge illegal upfront fees while promising to enroll borrowers in free federal consumer protections, including income-driven repayment plans.

The Bureau has made it a priority to take action against companies that are engaging in illegal student loan servicing practices. Earlier this year, the CFPB announced that its oversight work ended a range of illegal practices at certain student loan servicers, as identified by the Bureau’s supervisory program. The CFPB will also continue to monitor the student loan servicing market and intends to explore potential industry-wide rules to increase borrower protections. Today’s announcement builds on an interagency framework for market-wide reform announced in September 2015 in coordination with the Department of Education and Department of the Treasury.

“The Obama Administration continues to look for ways to make college more affordable and accessible for all families. A college degree is one of the best investments a student can make in his or her future, and it remains the clearest path to the middle class,” said U.S. Secretary of Education John B. King Jr. “We want student borrowers to know that they have the support they need to manage their debt and navigate the options available to them to pay back their loans.”

Student Loan Initiatives from the Department of Education and the Department of the Treasury

Today, the Department of Education and the Department of the Treasury, in consultation with the Bureau, also announced further actions aimed at protecting student loan borrowers:

- Student loan borrowers’ rights and expectations: The administration, in consultation with the Bureau and informed by work with Illinois Attorney General Madigan and other state law enforcement officials, has released a series of new student loan borrower rights and expectations . This provides a framework to help ensure borrowers with loans owned by the Department of Education are treated fairly and that the student loan repayment process sets these borrowers up to succeed. The Bureau continues to emphasize that no consistent, market-wide federal standards exist for conduct of student loan servicers. With this framework, the agencies have taken another step toward improving the delivery of service for millions of student loan borrowers.

- Strengthening student loan credit reporting: The administration, in consultation with the Bureau, is working with the credit reporting industry to develop guidance for servicers, lenders, and others that furnish data to the credit reporting companies. This effort will help determine how best to report student loan data to ensure that credit reporting for student loans fairly, consistently, and accurately reflects repayment activity. The Department of Education will implement this effort in the months ahead. Read more about this initiative.

Student loan borrowers can get more advice on student loan repayment options by using the CFPB’s Repay Student Debt tool. This interactive resource offers a step-by-step guide to navigate borrowers through their repayment options, especially when facing default. Student loan borrowers experiencing problems related to repaying student loans or debt collection can submit a complaint to the CFPB. More information is at https://www.consumerfinance.gov/students.